The World Does Not Wait for Small States

Bangladesh is not a passive audience to global events. It is a country of 170 million people, strategically positioned at the head of the Bay of Bengal, deeply integrated into global trade through a garment industry that dresses much of the world, and extraordinarily exposed to the forces — climate, geopolitical, economic — that are reshaping the international order. When the United States announces sweeping tariff changes, or when the European Union revises its trade preference architecture, or when Myanmar's civil war prevents the repatriation of a million refugees, or when global sea levels rise by another millimetre, Bangladesh feels the consequences with an immediacy that more insulated countries do not. Understanding the global events that shape Bangladesh's future is not an academic exercise. It is the essential context for understanding Bangladesh itself.

Several international developments that appear, on the surface, to be stories about other countries are in practice stories about Bangladesh too. Four of them define the country's strategic environment in 2025 and 2026 with particular force: the restructuring of global trade under Trump-era protectionism; Bangladesh's imminent graduation from Least Developed Country status and its implications for EU market access; the ongoing Myanmar civil war and its effects on Rohingya repatriation; and the accelerating climate crisis that is physically transforming Bangladesh's geography. Each is a global story. Each lands in Bangladesh.

Trump's Trade Nationalism: The $8 Billion Question

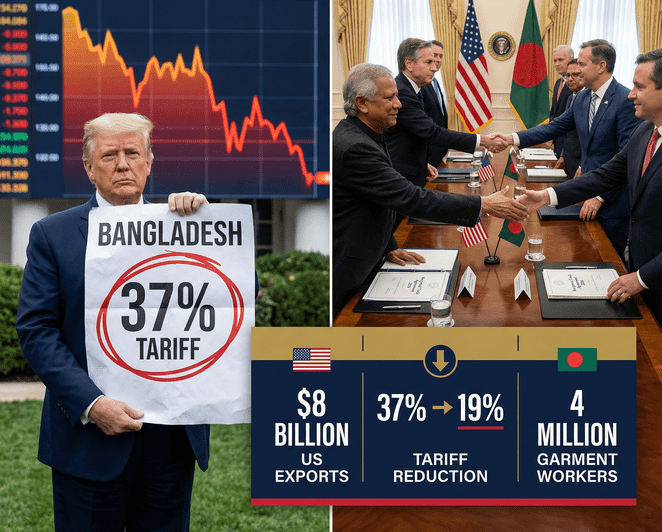

When Donald Trump announced his "Liberation Day" tariff package on April 2, 2025, imposing reciprocal tariffs on 157 countries, Bangladesh faced one of the most consequential trade policy shocks in its history. The initial rate — 37 percent on Bangladeshi exports, subsequently revised to 35 percent in July — compared with a prior average of approximately 15 percent. For a country that exports approximately $8 billion annually to the United States, with more than $6 billion in garments, the arithmetic was stark: a doubling of the effective duty on its most important export sector in its most important single market.

The context matters. Bangladesh's garment industry employs over four million workers, the majority of them women. The ready-made garments sector accounts for approximately 81.5 percent of Bangladesh's total export earnings and around 10 percent of GDP. When US retailers absorb a tariff shock and respond by placing more conservative orders, the consequence is not an abstract trade statistics revision — it is reduced factory hours, deferred wages, and potential layoffs for millions of workers in Dhaka, Chittagong, and Gazipur. The Political Research Institute of Bangladesh estimated that while Bangladesh's exporters might retain relative competitiveness against harder-hit rivals (Vietnam faced 46 percent, Cambodia 49 percent), the overall impact remained uncertain because reduced trade flows from retaliatory tariffs were damping global demand across the board.

Bangladesh's diplomatic response was vigorous. An emergency council was convened within days of the announcement. Chief Adviser Muhammad Yunus engaged directly with Washington. A key concession — increased imports of US goods to reduce the bilateral trade deficit — became the central negotiating offer. By February 2026, Bangladesh and the United States had concluded an Agreement on Reciprocal Trade reducing the tariff rate to 19 percent, with selected products potentially eligible for zero percent rates. Bangladesh committed to preferential market access for US agricultural and industrial goods, data transfer liberalisation, and intellectual property protections. The deal was welcomed domestically as a diplomatic victory, though analysts noted the commitments made represent real constraints on policy space for future governments — and that the US Supreme Court's ruling that IEEPA-based tariffs were illegal added ongoing legal uncertainty about the entire framework.

The structural lesson Trump's tariff policy delivered to Bangladesh is one the country had long known intellectually but not yet sufficiently acted upon: concentrating 84 percent of export earnings in a single sector (garments) and directing approximately a fifth of exports to a single country (the US) creates a vulnerability that no amount of diplomatic skill can fully offset. Export diversification — into pharmaceuticals, leather, light engineering, IT services — and market diversification — into the Gulf, ASEAN, Africa — are not just long-term aspirations. They are, after 2025, urgent strategic necessities.

LDC Graduation: The Tariff Cliff of 2026

The Trump tariff shock arrived simultaneously with a different but structurally related challenge: Bangladesh's scheduled graduation from Least Developed Country status on November 24, 2026. For decades, Bangladesh's garment export success has been built partly on preferential market access — most importantly the European Union's Everything But Arms scheme, under which Bangladeshi garments enter the EU duty-free. As a graduating LDC, that access phases out. Post-graduation, Bangladesh faces standard EU MFN tariffs exceeding 11 percent on apparel unless it successfully qualifies for the GSP+ scheme, which offers duty-free access to 66 percent of EU tariff lines.

The problem is that GSP+ eligibility for garments carries a structural barrier: a beneficiary country's share of the relevant product category's EU imports cannot exceed 6 percent. Bangladesh's current apparel market share in the EU is well above that threshold — meaning its garment exports would not automatically qualify for GSP+ duty-free treatment even if Bangladesh fulfils all the other conditions. The WTO's estimates suggest Bangladesh could forfeit up to $8 billion in annual export earnings — approximately 14 percent of total exports — when LDC preferences fully lapse. EU and UK GSP schemes provide a three-year transition period, meaning the full tariff cliff arrives in November 2029. The next most generous scheme — GSP+ for non-apparel products — remains available and valuable, but the core garment competitiveness challenge is significant.

Bangladesh formally requested a three-year deferral of LDC graduation, citing domestic disruptions — financial sector irregularities, foreign exchange reserve pressure, high inflation, and the political changes following the 2024 uprising — that had "severely disrupted" the preparatory period. The UN Committee for Development Policy is considering the request. The commerce minister of the newly elected BNP government signalled the administration would pursue all available steps to delay graduation. The EU ambassador to Bangladesh offered encouraging words in December 2025, noting that Bangladesh "can benefit from the EU's GSP+ scheme" and welcoming Bangladesh's recent ratification of key ILO conventions on labour rights.

LDC graduation is paradoxically both a badge of development achievement — reflecting the genuine socioeconomic progress Bangladesh has made over five decades — and a potential trap in which success creates vulnerability. The global institutional architecture of trade preferences was designed to help poor countries grow; it was not fully designed for the transition out of those preferences. Bangladesh's experience will be closely watched by other graduating LDCs, and its success or failure in navigating the transition will shape how the international community thinks about graduation support mechanisms.

Myanmar's Civil War and the Rohingya Impasse

Bangladesh hosts approximately 1.2 million Rohingya refugees — the world's largest stateless population, driven from Myanmar by military violence in 2017 and earlier waves of persecution. The Rohingya crisis is frequently discussed as a humanitarian issue. It is equally a geopolitical and economic one, whose resolution depends entirely on political developments in Myanmar over which Bangladesh has no control.

Myanmar's military junta, which seized power in the February 2021 coup, has since been engaged in a multi-front civil war against the National Unity Government, Ethnic Resistance Organisations, and People's Defence Forces. The conflict has intensified rather than resolved in 2024-25. In this environment, the conditions for safe, voluntary, and sustainable Rohingya repatriation — the only permanent solution that Bangladesh, the UN, and the Rohingya themselves have articulated — do not exist. Repatriation requires not only a ceasefire but the restoration of citizenship rights, the return of confiscated land, and safety guarantees that a military junta fighting for its own survival cannot credibly provide.

For Bangladesh, the consequences of this impasse compound annually. The Cox's Bazar camps — the largest refugee settlement in the world — consume significant government resources, create local economic strains in one of Bangladesh's poorest districts, and generate environmental damage including deforestation in the buffer zone adjacent to the Teknaf Wildlife Sanctuary. Funding from international donors has declined relative to the scale of need. The World Food Programme cut rations for camp residents in 2023 and again in 2024, citing funding shortfalls, with immediate nutritional consequences. Bangladesh has explored alternative arrangements — a relocation of some refugees to Bhasan Char island in the Bay of Bengal — but international human rights organisations raised concerns about the suitability and sustainability of island relocation.

The geopolitical dimension is significant. China, which has substantial economic interests in Myanmar through infrastructure projects and resource extraction, has positioned itself as a mediator in the Myanmar conflict. Bangladesh-China relations have been a balancing act throughout — China is Bangladesh's largest trading partner and major infrastructure investor, but China's mediation in Myanmar has consistently produced more process than result. The Arakan Army's growing military control over Rakhine State — the origin region of the Rohingya — creates a new political reality: any repatriation negotiation may eventually need to involve the Arakan Army, not just the junta, adding a further layer of complexity to an already intractable situation.

The Climate Crisis: Rewriting Bangladesh's Geography

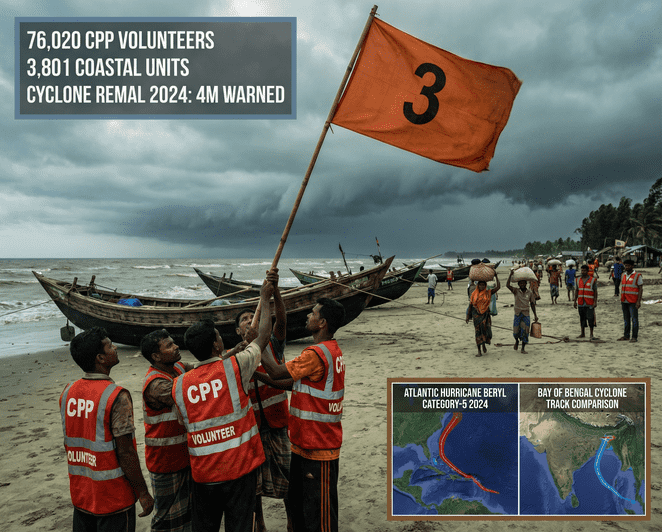

By 2050, Bangladesh is projected to lose 17 percent of its territory to rising sea levels, along with 30 percent of its agricultural land. By 2030, the World Bank estimates that nearly 90 percent of South Asia's population will be at risk of extreme heat, and nearly a quarter at risk of severe flooding. Bangladesh sits at the intersection of multiple climate vulnerabilities: a low-lying delta exposed to sea-level rise and storm surge; a monsoon-dependent agricultural system increasingly disrupted by erratic precipitation; and a position at the head of the Bay of Bengal, which is warming and intensifying tropical cyclones.

The climate crisis is not a future threat for Bangladesh. It is a present reality. Saltwater intrusion into coastal aquifers is already affecting freshwater supply and agricultural productivity in the Sundarbans region. River erosion displaces tens of thousands annually. Cyclone frequency and intensity have increased relative to historical patterns. The 2024 monsoon season produced devastating floods that affected an estimated 18 million people across Bangladesh, compounding the effects of Cyclone Remal's landfall in May.

Global climate negotiations directly determine the scale and nature of international support available to Bangladesh for adaptation and mitigation. The fracturing of the global climate consensus under Trump's second term — the administration announced US withdrawal from the Paris Agreement — removes the world's largest historical emitter from the framework through which climate finance, technology transfer, and emission commitments flow. For Bangladesh, which contributes less than 0.5 percent of global greenhouse gas emissions but bears a disproportionate share of climate consequences, this is not a policy disagreement but a fundamental injustice with immediate material implications. The Loss and Damage Fund established at COP27 and operationalised at COP28 represents a hard-won institutional mechanism for climate-vulnerable countries — but its capitalisation remains far below what Bangladesh and its peers need.

The World Bank's November 2025 South Asia climate resilience report found that about one-third of climate-related losses in Bangladesh could be avoided if the private sector were able to move resources and investments where needed most. The report emphasised that even with tight government budgets, expanding access to finance, improving transport and digital networks, and ensuring flexible social support systems could significantly enhance resilience. Bangladesh's CPP volunteer network and cyclone shelter infrastructure demonstrate what community-based adaptation can achieve. Scaling these models, financing them sustainably, and embedding them in a global architecture that shares the cost of adaptation fairly are the international policy challenges on which Bangladesh's physical future depends.

What Bangladesh Needs from the World

The four global stories examined here — US trade nationalism, LDC graduation, Myanmar's civil war, and the climate crisis — share a structural feature: they are all produced substantially by decisions made in other capitals and other boardrooms, and they all land disproportionately on Bangladesh. This asymmetry — between the location of decisions and the location of consequences — is the fundamental condition of Bangladesh's engagement with global affairs.

What Bangladesh needs from the world is not charity. It is fairness. Fair trade architecture that provides transition pathways for graduating LDCs rather than tariff cliffs. Fair burden-sharing on climate finance that reflects the relationship between historical emissions and current vulnerability. Fair engagement with the Rohingya crisis that maintains funding, presses Myanmar diplomatically, and explores repatriation frameworks that actually function. And fair acknowledgment that a country contributing so comprehensively to global supply chains — dressing the world, manufacturing for its largest retailers — deserves a seat at the tables where the rules governing those supply chains are made.

Bangladesh has spent five decades demonstrating that a country with limited natural resources, high population density, and severe climate exposure can develop rapidly through human capital investment, export-led growth, and institutional innovation. The next decade will test whether the international system is capable of supporting that trajectory — or whether the converging pressures of protectionism, preference erosion, unresolved humanitarian crises, and accelerating climate change produce outcomes that reverse it.

win-tk.org is a wintk publication covering global and regional affairs with a focus on Bangladesh and South Asia.